Table of Content

Debt settlement, on the other hand, is where a company negotiates on your behalf in an effort to get your creditors to accept a reduced amount in return for paying off the debt. This often involves the creditor agreeing to forgive some or all of the interest charges and penalties that have accumulated on a past-due debt. The more you pay to your lender, the higher your equity grows.

Second, you may be able to set up a consolidation loan that lets you pay off your debt over a longer time than your current creditors will allow, so you can make smaller payments each month. That's particularly helpful if you can combine it with a lower interest rate as well. With a cash-out refinance, you replace your existing mortgage loan with a larger mortgage loan, and the difference is disbursed to you as a lump sum.

Debt Relief: Understand Your Options and the Consequences

Experts recommend that you only use your home’s equity for emergency situations, such as unexpected medical bills or emergency debt consolidation. You have two options if you choose to tap into your home’s equity. You can get a home equity loan or a home equity line of credit . Before applying for a mortgage, double down on your budget and aggressively pay down your debt balances.

If you have good credit, it can be significantly lower than the rates on your credit cards. What’s more, the rate won’t change (which can happen with credit cards and other adjustable-rate lending products). Other financing options that consolidate debt require you to borrow against something. You’re not borrowing against your home, your 401, or your life insurance policy. This means that you’re not forced to put yourself into a riskier financial position just to get out of debt.

Is a Home Equity Loan the Best Way to Consolidate Debt?

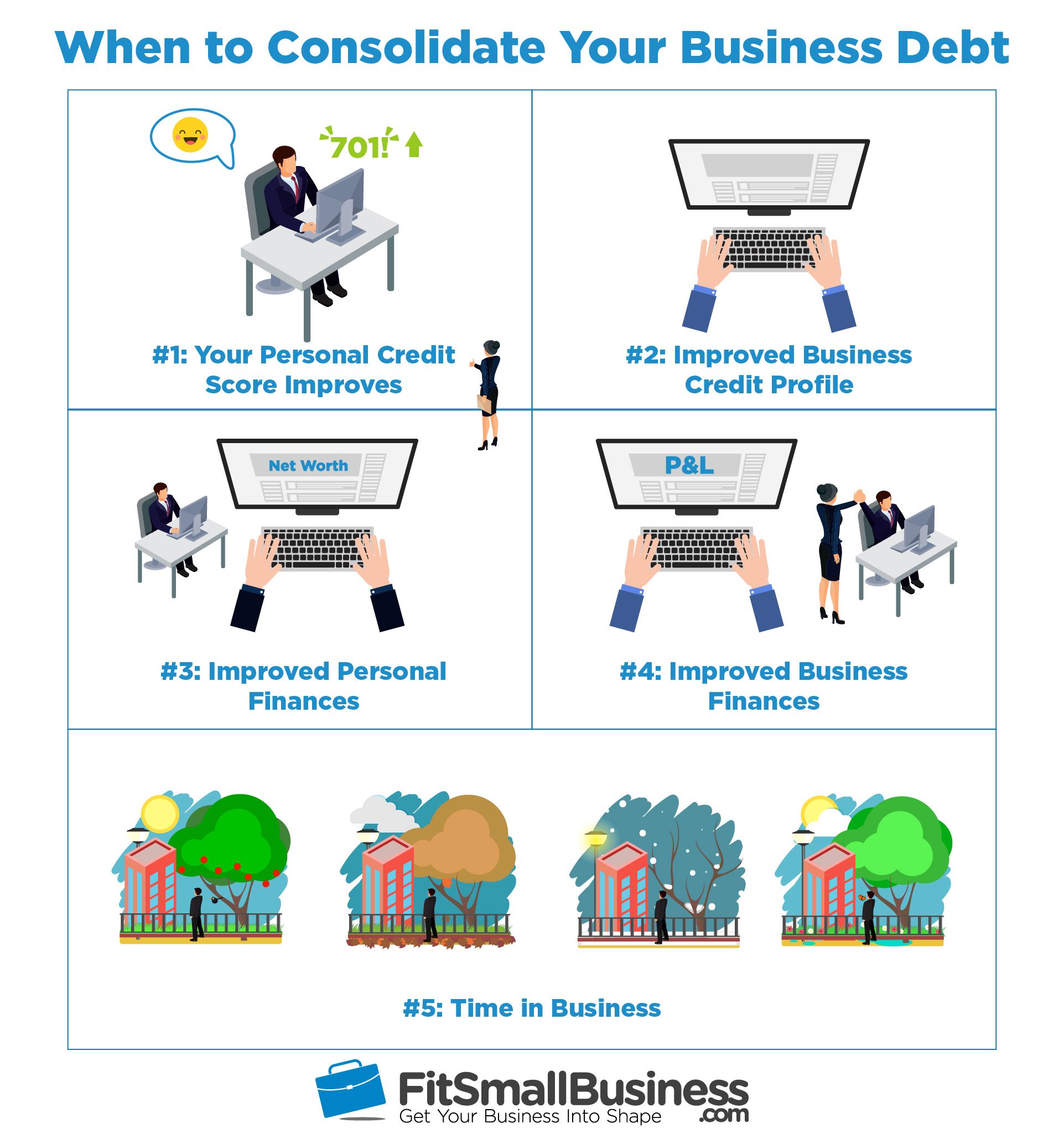

The online lender also has a minimum annual income requirement of $45,000 for its debt consolidation loans. SoFi also emphasizes having a healthy debt-to-income ratio, which shows that borrowers have enough money left over each month to pay off their SoFi personal loan. But with so many debt consolidation companies to choose from, picking the right lender can feel like an overwhelming task. To help you decide, we’ve reviewed the best debt consolidation loan lenders. We evaluated each debt consolidation company on a variety of factors including APRs, fees, loan amounts, repayment terms, and credit score requirements.

Unlike many other online lenders, SoFi doesn’t charge any origination fees or late fees, though borrowers will continue to accrue interest on late payments. Neither does the platform charge prepayment penalties, meaning you can pay off your loan anytime without negative consequences. Full application requirements often include proof of employment, gross monthly income, monthly mortgage or rent payment amount, and recent W-2s or tax returns. In some cases, depending on the lender and how the loan proceeds are dispersed, you may also be required to provide account information for the debts to be paid off.

Best for Bad Credit

And, while LendingClub does not offer the fastest funding time, it will directly pay your creditors so you don’t have to worry about the logistics of debt consolidation. Unlike other types of debt consolidation, refinancing involves trading one loan for a different, better loan. Consolidating with a personal loanor credit card balance transferoften means rolling multiple loans into a different, better loan. Just keep in mind that the interest rate you’ll receive depends upon a few factors, such as credit score and your individual financial situation.

This is because, unlike credit cards, medical loans and other forms of debt, personal loans often come with lower interest rates—especially if you have good to excellent credit. Many lenders also offer direct payments to third-party creditors, so you won’t have to worry about the logistics of consolidating your other debts. Compare your financial situation to the criteria above to decide whether your home’s equity makes sense for you.

Should I Consolidate Debt Before Buying a Home?

By making a $1,000 payment on the card each month, you'll have it paid off before the promotion expires. If you allow it to expire, though, the interest will jump up to a standard rate, which can easily be 20% or more. Opinions expressed here are author's alone, not those of any bank, credit card issuer or other company, and have not been reviewed, approved or otherwise endorsed by any of these entities. All information, including rates and fees, are accurate as of the date of publication and are updated as provided by our partners. Some of the offers on this page may not be available through our website. If you're considering debt consolidation, it's best to carefully evaluate your financial situation and research your options to determine if it's the right solution for you.

This may influence which products we write about and where and how the product appears on a page. Find out how much debt you have, how much you need to pay it off and the method that allows you to do this with the least amount of risk. You’ll get lower HELOC interest rates because your home is used as collateral. Credit cards aren’t backed by any physical property, which is one of the reasons interest rates are so high. The first step to using your home as part of a solution to this problem is understanding what home equity is. Home equity is the difference between what your home is worth and what you owe to the lender.

You must keep track of multiple due dates and pay each debt on time to avoid additional interest, fees and penalties. Because you need to consider these factors, and more, it is important to sit down and talk to a mortgage lender before you make your next move. A loan officer will ask you questions about your short- and long-term financial goals and your present situation and then, provide you with options so you can make informed decisions. We specialize in meeting each client’s unique refinancing needs, and we fully understand that everyone’s mortgage situation is different.

This may include reviewing your budget and changing some of your spending habits. Researching the lender itself is another important step when considering a debt consolidation loan. You’ll want to be sure to select a lender that has a good reputation and has received positive reviews from previous borrowers.

By definition, a loan has a set date when your payments start and a set debt when your payments will end. You get off the credit card debt treadmill where you diligently make payments, but your balances never seem to go down. Debt consolidation is recommended for homeowners who have a good deal of equity in their homes that can be tapped to pay off other high-interest debts . Since the goal is to refinance into a low-interest mortgage, borrowers with a high credit score are in the best position to take advantage of this refinance type. Interest rates on home equity loans and home equity lines of credit are typically lower than those on credit cards.

No comments:

Post a Comment